.webp)

State of HOA management in 2026

The HOA industry is growing, and it is under real pressure at the same time. There are now approximately 377,000 community associations in the United States, housing nearly 80 million Americans. Insurance premiums are up sharply, reserve funding shortfalls are forcing large special assessments in some communities, and new legislation in Florida and California has added compliance obligations boards were not carrying two years ago. None of that means the model is broken. Communities that understand their numbers, communicate clearly, and use the right tools are managing well. The ones that are struggling tend to share the same problem: they deferred hard decisions for too long.

Ask any HOA board member what 2026 feels like and the answer is usually some version of the same thing: more complicated, more expensive, and harder to explain to homeowners who want to know why their dues went up again. Those are real problems. What tends to be missing is a clear picture of what is driving them and, more importantly, which communities are actually handling this well and what they are doing differently.

This overview draws on current data from the Foundation for Community Association Research, the US Census Bureau, and industry legal and insurance sources. The trends are real and the challenges are significant. But the most important thing the data shows is not that the industry is in crisis. It is that the gap between well-run communities and struggling ones is widening, and the difference is rarely budget size.

HOA Industry Growth: Size and Scale in 2026

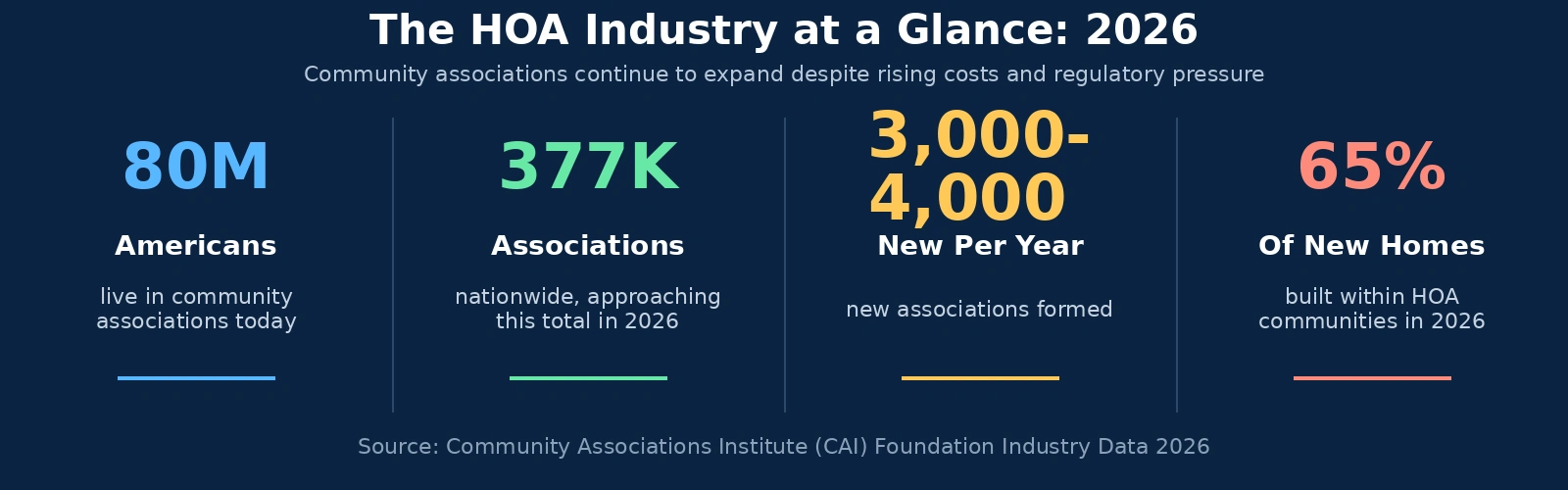

One thing that is not in doubt in 2026 is that the HOA model is growing. The Foundation for Community Association Research projects approximately 377,000 community associations across the US this year, up from about 373,000 at the end of 2025, with 3,000 to 4,000 new associations forming every year. Nearly 80 million Americans now live in HOA-governed communities, accounting for about one-third of all US housing stock (source: Foundation for Community Association Research, 2026 Outlook).

That growth is structural, not cyclical. Developers building at the higher end of the market, where most new construction is concentrated, are building into planned communities with shared governance. A 2025 Foundation for Community Association Research report found that 66% of newly completed homes are in community associations. A Realtor.com analysis from early 2026 found that 44% of homes currently listed for sale carry an HOA fee. If you are a homebuyer almost anywhere in the Sun Belt or on either coast, avoiding an HOA has become genuinely difficult.

Sources: Foundation for Community Association Research 2026 Outlook; US Census Bureau 2024 American Community Survey; Realtor.com 2026 market analysis.

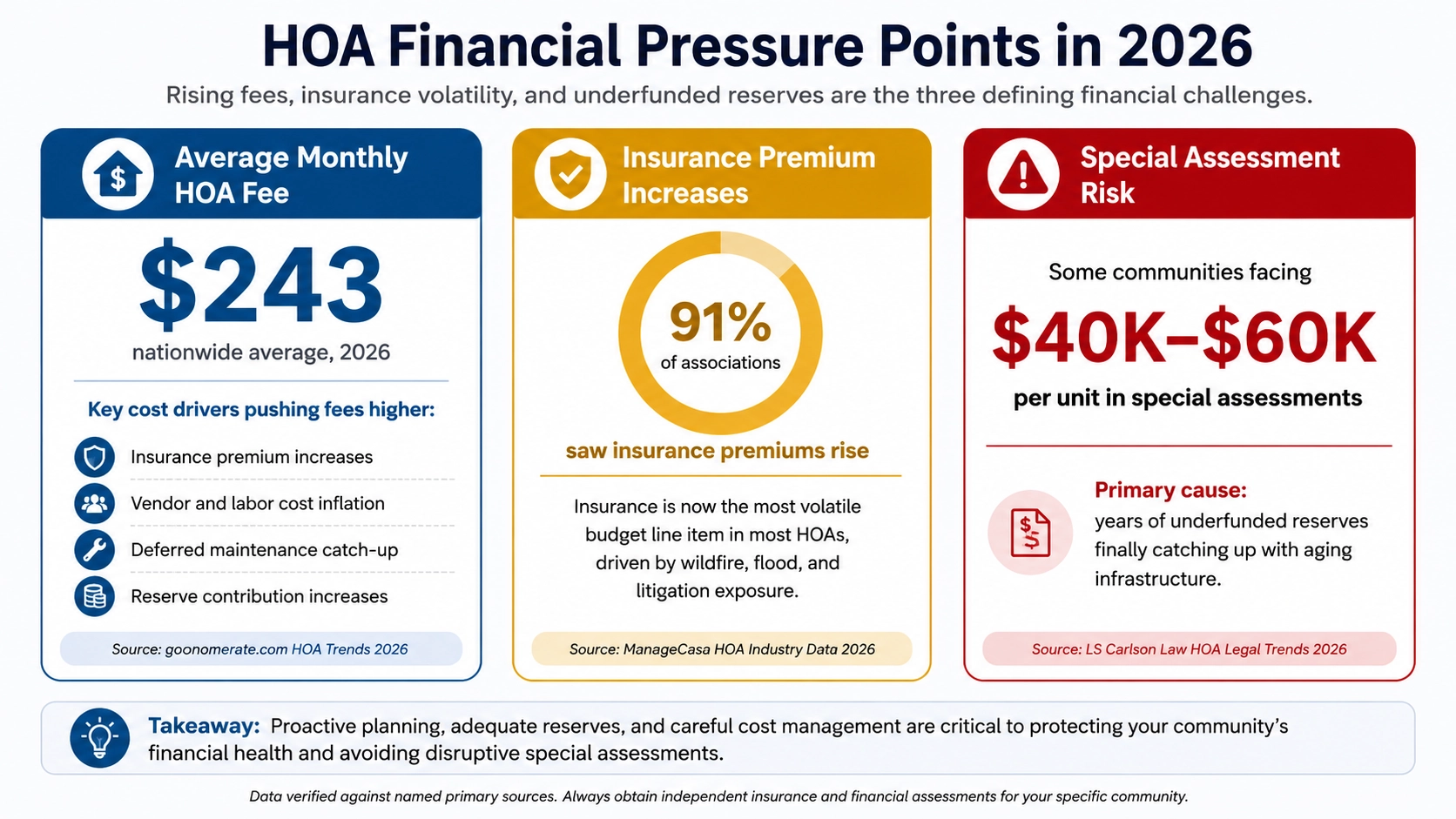

The national median HOA fee, per the US Census Bureau's 2024 American Community Survey, is $135 per month. That number tends to surprise people, because it is lower than the fees most boards are actually working with. The median is pulled down by the large number of small associations with minimal amenities and low common area costs. About 5.6 million households pay under $50 per month. But roughly 3 million pay over $500, and in coastal Florida, HOA fees in some communities now make up more than a quarter of total monthly housing costs. Location, property type, amenity footprint, and above all insurance exposure explain most of the variation.

HOA Fee and Financial Trends: Rising Costs Across Every Budget Line

Here is what is true about HOA finances in 2026: almost everything costs more than it did three years ago, and the communities that are in the most pain are generally the ones that tried to hold the line on assessments for too long. Insurance went up. Vendor contracts went up. Labor went up. And for associations that deferred reserve contributions during the low-interest-rate years because the money seemed better used elsewhere, those decisions are now arriving as bills.

Insurance premiums are the biggest single pressure point

Insurance is where the budget conversation starts in most communities right now, and for good reason. A survey by the Foundation for Community Association Research found that 91% of community associations reported an unexpected increase in expenses, with insurance identified as one of the top drivers, second only to management costs (source: Clark Simson Miller, Rising HOA Insurance Rates). Nationally, industry projections put average HOA insurance premium increases at around 8% in 2026. But that national average is doing a lot of averaging. Communities in coastal Florida, wildfire-exposed California counties, and hurricane-prone areas of the Southeast are looking at increases of 25% to 50% or more, with some markets seeing carriers exit entirely (source: HOA ENC, Top HOA Issues for 2026).

The underlying drivers are not going away quickly: reinsurance cost surges, more frequent severe weather events, inflation in construction and labor, and a shrinking pool of carriers willing to write community association policies in high-risk markets. For California associations specifically, a November 2025 analysis from Silver Creek Association Management recommended treating a 10% premium increase as the minimum budget assumption for 2026, not a worst case.

Practical note for boards facing renewal: work with a broker who specializes in community associations and submits to multiple carriers simultaneously. In a hardening market, the spread between the best and worst available quotes is significant, and a specialist broker knows which carriers are still writing aggressively and which have quietly tightened their appetite.

Reserve funding shortfalls are creating special assessment risk

The reserve funding problem is not complicated to understand, but it is uncomfortable to confront. Associations that held assessments flat for years, or that raided reserves for operating expenses, are now discovering that the major components they deferred funding for, roofs, HVAC systems, pool decks, elevators, have not gotten any cheaper. In some Florida condominium communities, where post-Surfside legislation has accelerated structural inspection requirements and forced reserve funding to levels that were previously optional, the catch-up has been severe. Some communities are facing special assessments of $40,000 to $60,000 per unit (source: LS Carlson Law, HOA Legal Trends to Watch in 2026).

This is not only a Florida or high-cost-market problem. As WTOP reported in March 2026, the pattern is happening across the country: homeowners moving into communities with underfunded reserves and then getting hit with large assessments shortly after. "People are getting payment shocks when they move in, and in three months, the assessment doubles or they get hit with a special assessment," said David Diestel, CEO of FirstService Residential, cited in WTOP, March 2026.

The only reliable way to know where you actually stand is a current reserve study. If your last one is more than three years old, the numbers you are budgeting against may bear little resemblance to what you actually owe. For a full breakdown of reserve fund structure, funding levels, and how to read a reserve study, see the HOA reserve funds guide.

Homeowner expectations around financial transparency are rising

Raising dues is hard. Raising dues without explaining why, in clear terms that a homeowner who does not attend board meetings can understand, tends to generate the kind of conflict that follows a community for years. What the data consistently shows is that homeowners are not necessarily opposed to paying more when costs genuinely require it. What they are opposed to is being surprised. Boards that communicate proactively, that show their work on the budget and explain what drove the increase, face significantly less friction than those that post a notice and hope for the best. The stakes are higher in 2026 because the dollar amounts are larger. The HOA financial transparency guide covers the what, the how often, and the format that works.

HOA Regulatory Trends in 2026: Homeowner Protections Are Expanding

The regulatory direction in 2026 is not ambiguous. Across the US, the trend is toward stronger homeowner protections, more financial disclosure, and tighter reserve funding requirements. Florida and California have attracted most of the attention, but they are leading indicators, not outliers. If you operate in Nevada, Colorado, Washington, or Virginia, your state has active HOA legislation either already in effect or moving through the process.

Florida: HB 1203 and the structural inspection mandate

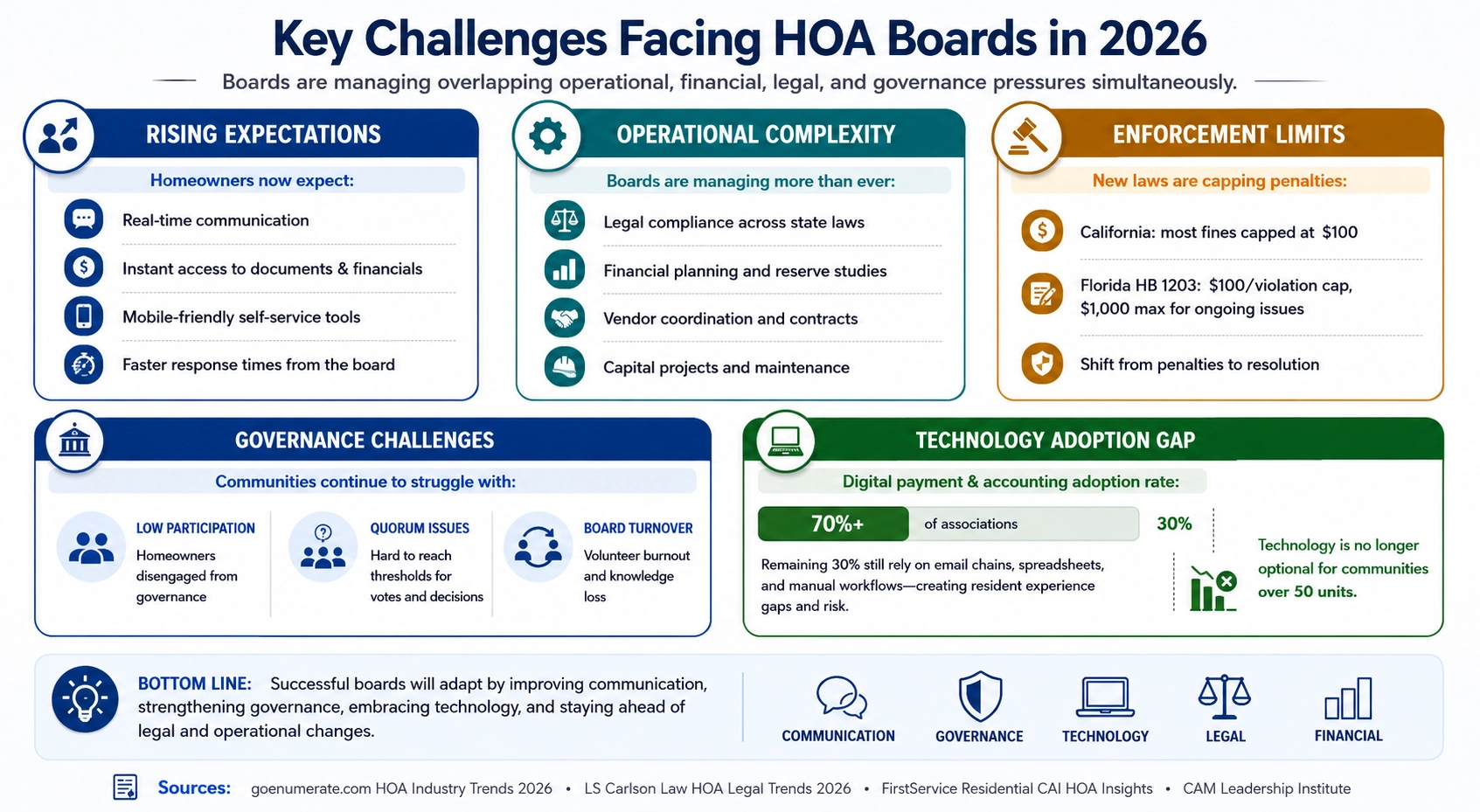

Florida's HB 1203 and the companion HB 1021, which took effect in 2024, represent the most significant changes to Florida HOA law in decades. Fine caps now sit at $100 per violation with a $1,000 maximum for ongoing issues. Restrictions on personal vehicle parking in driveways are prohibited. And for condominium associations, the structural inspection and reserve funding requirements driven by the 2021 Surfside collapse have fundamentally changed what adequate reserve funding means in practice. Boards that were previously compliant under the old standards may not be under the new ones. The Florida HB 1203 compliance guide covers what changed, what is required, and what the timelines look like.

California: fine caps and enforcement shifts

California capped most HOA fines at $100 per violation effective 2024, a change that has forced a genuine rethink of enforcement strategy in many communities. When the fine is capped at $100, it stops functioning as a deterrent for homeowners who would rather pay the fine than comply. The practical result is that boards in California are shifting toward resolution-based approaches, which means more communication, more documented outreach, and less reliance on the fine schedule as the first line of response. The California HOA law changes 2026 article covers the current Davis-Stirling landscape in detail.

The broader national trend

The pattern running through all of this is the same one. Legislators in state after state are looking at HOA governance and deciding that the balance of power needs to shift toward homeowners. That is the direction and it is not reversing. For boards operating in any state with active HOA legislation, staying current is not something that can wait for the annual attorney letter. It requires ongoing attention, and increasingly, professional support or dedicated tracking tools to manage it reliably.

The HOA accounting guide's state requirements table covers eight states in detail, including statutes, audit requirements, and reserve study mandates: HOA accounting and financial management guide.

Key Challenges Facing HOA Boards in 2026

Most boards going into 2026 were already managing a full plate. Rising costs and tightening regulations did not replace the existing workload, they landed on top of it. The result is that the people running most community associations, whether volunteer board members or professional managers, are being asked to do significantly more with the same bandwidth they had three years ago.

Board workload and burnout are growing

The job of running an HOA has changed materially over the past decade. Legal compliance, vendor coordination, capital project planning, financial reporting, resident communication, and enforcement have all grown in complexity, and all of it still has to be managed by people who signed up to serve their community, not to run a small corporation. Manager burnout and board member turnover are rising as a result. The communities that hold onto good people longer tend to be the ones where the operational load is distributed sensibly and where technology handles the administrative layer so that human attention can go where it actually matters.

Low meeting participation and quorum difficulties

Getting homeowners to show up, whether to a meeting, a vote, or even a survey, remains one of the most persistent operational frustrations in community association management. Reaching quorum for required votes on budget approval, special assessments, rule changes, and elections is a recurring problem in communities of every size. Electronic voting has helped where it has been adopted. Florida and California have both formally authorized it for HOA elections, and participation rates in communities that have deployed digital voting tools have generally improved. The friction of requiring physical attendance was always doing a lot of the work in keeping participation low.

Governance conflict is increasing

Board and homeowner conflict is measurably up in 2026. Higher fees, more enforcement activity, and homeowners who are significantly better informed about their rights than they were five years ago make for a more challenging governance environment. The communities that navigate this well tend to share a few consistent habits: they communicate before homeowners have to ask, they document decisions clearly enough that the reasoning is transparent, and they treat resident access to information as a feature rather than a burden. The ones that struggle tend to reach for enforcement first and communication second, and the results are predictable.

Vendor management complexity

The cost and complexity of managing vendors has gone up alongside everything else. Insurance certificate requirements have tightened. Contract renewal pricing has increased. Competitive bidding thresholds that seemed generous a few years ago are now being hit more often. For associations managing multiple vendors across common area maintenance, a structured work order system is increasingly the difference between documented accountability and a shared spreadsheet that nobody trusts. For a breakdown of what that looks like in practice, see the HOA work order software guide.

Technology and AI in HOA Management: Adoption Is Accelerating

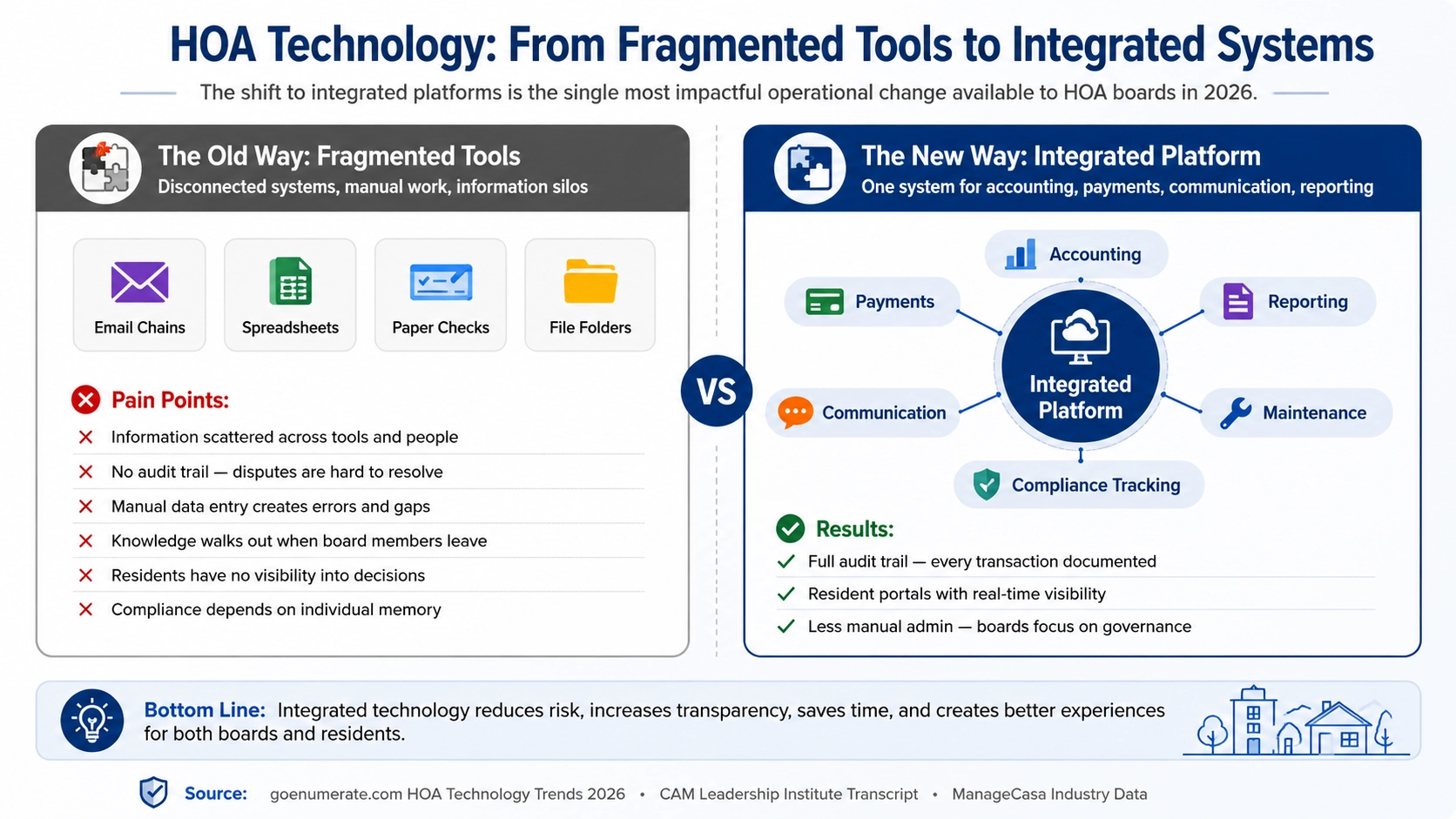

The honest version of the technology story in 2026 is not that every community has gone digital. It is that the gap between communities using integrated platforms and those still running on spreadsheets and email threads is getting wide enough to matter operationally. Most associations managing 50 or more units are using dedicated software for at least some functions. The ones that have consolidated those functions into a single platform are operating noticeably more efficiently than the ones running four separate tools that do not talk to each other.

The move from fragmented tools to integrated platforms

For most of the last decade, community associations adopted technology the way most small organizations do: one problem at a time, one tool at a time. A separate system for accounting, a different one for communications, another for work orders. The result was a collection of tools that each required their own data entry and produced their own reports, with no single place where the board could see the full picture. The shift happening now is consolidation: accounting, assessment collection, work orders, resident communication, violation tracking, and board document storage increasingly living in one system. The operational benefit is less about any single feature and more about the elimination of the manual handoffs between tools.

For self-managed communities in particular, this shift changes what is actually achievable with volunteer bandwidth. Monthly financial reporting, automated payment reminders, and maintenance request routing handled by the software means board members spend their meeting time on decisions, not on trying to catch up on what happened since the last meeting.

AI is beginning to appear in operational workflows

AI in HOA management is real but early in 2026. The most common applications are automated triage of maintenance requests, which routes by urgency and category without requiring a manager to read and sort every submission; anomaly detection in financial records, which flags unusual transactions or budget variances for board review rather than waiting for month-end; and predictive budgeting tools that model reserve fund trajectories under different contribution scenarios. Larger management companies are building internal AI tools for these functions. For boards on platforms that have integrated AI features, the practical result is earlier visibility into problems that would previously have been invisible until the numbers were already off.

Resident expectations around digital experience

Homeowners in 2026 do not think of a resident portal as a nice extra. They expect to check their account balance, view association documents, submit a maintenance request, and pay their dues from their phone, without calling anyone. Communities that still send paper notices for everything and route all requests through email are creating friction that shows up as inbound call volume, meeting complaints, and reduced satisfaction. The communities that have moved to a well-designed homeowner portal and proactive digital communication are seeing the difference on both sides: lower administrative overhead for the board and fewer complaints from residents who feel left in the dark.

2026 Outlook: What to Expect in the Year Ahead

The direction of the HOA industry in 2026 is not a secret: higher costs, more regulation, more complexity, more homeowner scrutiny. None of that is going to reverse. But none of it automatically makes a community harder to run well. The boards that are navigating 2026 effectively are not necessarily the best-funded or the largest. They are the ones where someone actually understands the reserve study, where fee increases get communicated before they land on the invoice, and where the operational layer is handled efficiently enough that volunteer energy can go toward the decisions that actually require human judgment. That is not a technology story or a compliance story. It is a management story, and it is the same story it has always been.

ManageCasa: built for community association management

ManageCasa covers the full HOA operations workflow, including accounting, automated assessment collection, work order management, resident communication, board reporting, and homeowner portals, alongside rental management for mixed portfolios. For boards and managers looking to reduce administrative workload and improve resident transparency, learn more at managecasa.com/capabilities/management

Content Writer

Dann is a real estate and property management content strategist specializing in HOA operations, financial management, and community governance. He works closely with industry professionals to produce accurate, practical guidance for property managers and HOA boards.