What is HOA accounting? HOA accounting is the systematic recording, tracking, and reporting of all financial transactions within a homeowners association. It covers dues collection, expense management, reserve fund oversight, budget planning, financial statement preparation, tax filing, and compliance with state HOA financial reporting requirements. Community association accounting differs from standard business bookkeeping because associations are nonprofit entities managing pooled homeowner funds under fiduciary obligations and legal governance requirements.

If you sit on an HOA board, you already know that managing a community involves far more than approving landscaping bids and enforcing parking rules. The financial side of the job is where things get genuinely complicated, and where the stakes are highest. Good HOA financial management touches every dollar that flows in and out of your community: dues collected from homeowners, vendor invoices paid on time, reserves set aside for future repairs, and taxes filed correctly every year.

Get it right and your community runs smoothly. Homeowners trust the board, property values stay healthy, and you are not scrambling for cash when the roof needs replacing. Get it wrong, and the consequences show up fast: surprise special assessments, deferred maintenance, and in serious cases, personal legal liability for board members.

This guide walks through everything boards and managers need to understand about HOA accounting services: the accounting methods, the chart of accounts structure, the financial reports, the fund structures, the compliance requirements, the cost of professional services, and the practical habits that keep an association financially solid. Whether your community is self-managed or works with a professional HOA management accounting firm, the principles here apply.

Why HOA Accounting Is Different From Ordinary Bookkeeping

Homeowners associations sit in an unusual spot financially. They are not businesses trying to turn a profit, but they handle money with the same level of complexity as many small companies. Every month, dues come in from dozens or hundreds of homeowners. Bills go out to landscapers, insurance carriers, utility companies, and property managers. Reserves need to be tracked separately and protected. Taxes need to be filed correctly. And all of it needs to be documented clearly enough that a board of volunteers can review it and explain it to the community.

Community association accounting adds another layer on top of ordinary bookkeeping: fiduciary duty. Every board member has a legal obligation to act in the financial best interest of the association. That means decisions about reserve funding, assessment collection, and vendor contracts are not just operational choices -- they carry legal weight. Sloppy bookkeeping leads to cash shortfalls, missed tax deadlines, and the kind of financial surprises that damage trust. Fraud is also a real risk in self-managed associations where the same person handling payments is sometimes the only one reviewing the accounts.

That combination of responsibilities is what makes homeowners association accounting its own discipline -- and why dedicated HOA bookkeeping services have grown significantly as a professional category. Boards are under more pressure than ever to deliver accurate, transparent financials, and many have found that outside professional help is simply the more reliable path.

The Three HOA Accounting Methods

Before any transactions get recorded, your association needs to decide how it will track them. The accounting method you choose determines what shows up on your financial statements, what an outside auditor will find, and whether your books meet Generally Accepted Accounting Principles (GAAP). It is worth getting this right from the start.

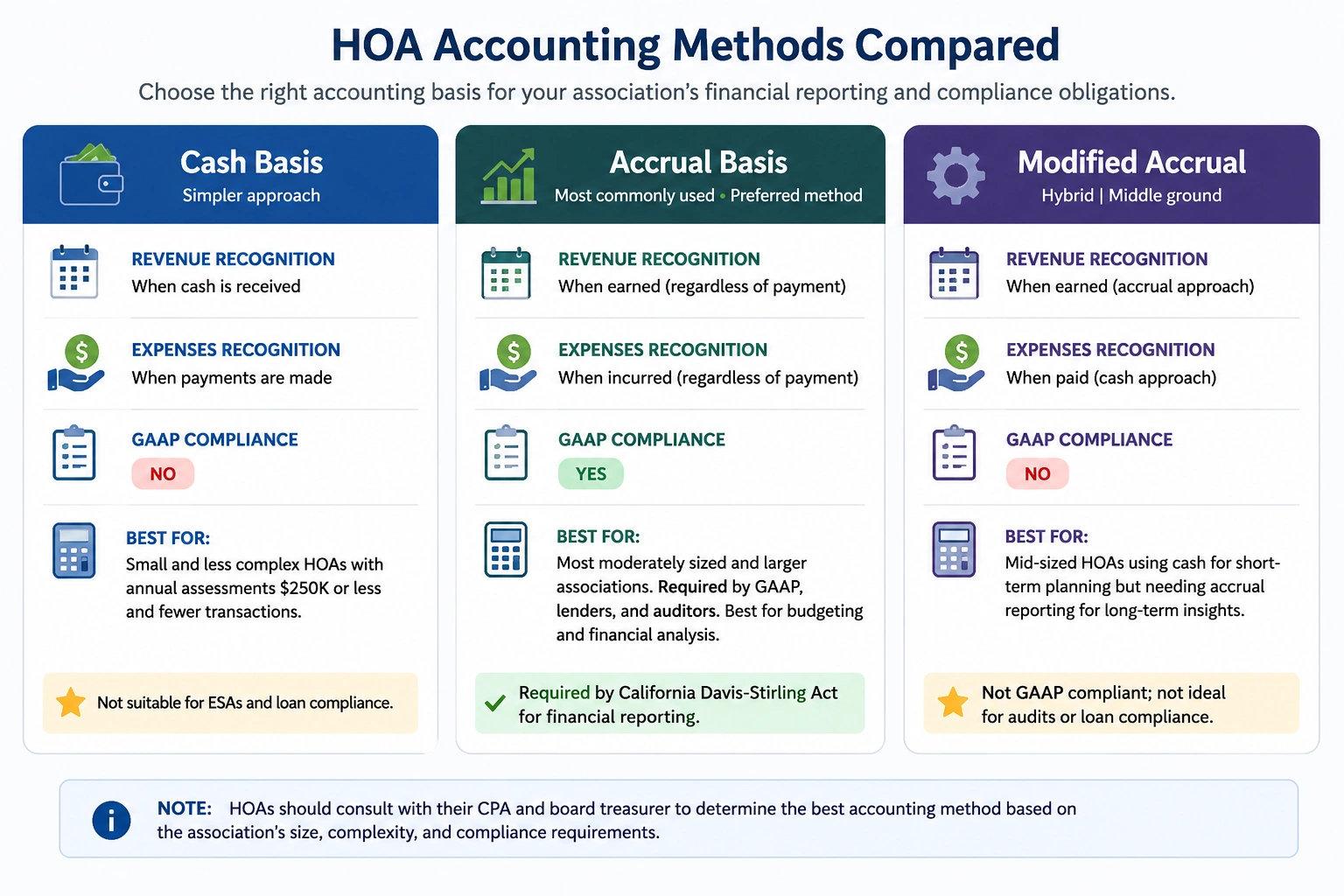

Cash basis accounting

Cash basis is the most straightforward approach. You record income when money arrives in the bank and record expenses when you write the check. Smaller self-managed associations often start here because it is easy to understand and requires minimal accounting infrastructure. The catch is that cash basis only shows you what has actually moved. Unpaid assessments and outstanding invoices are invisible until money changes hands, so your financial statements can look healthier or shakier than reality. Cash basis is also not GAAP-compliant, which matters if you ever need reviewed financials for a lender or outside auditor. Note: California law requires HOAs to use accrual basis when preparing their pro forma operating budget, regardless of the method used for internal tracking.

Accrual basis accounting

With accrual accounting, you record income when it is earned and expenses when they are incurred, regardless of when cash actually moves. If you bill homeowners for quarterly dues in January, that revenue is on the books in January, even if a few payments trickle in late. If a contractor does the work in December but sends the invoice in January, the expense belongs in December.

Accrual is the only method that conforms with GAAP, and it is what virtually every professional HOA accounting firm uses for final reporting. Accounts like Assessments Receivable and Accounts Payable appear on your balance sheet, giving you a complete, honest picture of what the community is owed and what it owes. If your association works with a CPA, plans to borrow money, or is subject to state reporting requirements, accrual basis is the standard you need.

Modified accrual basis accounting

Modified accrual, sometimes called modified cash basis, splits the difference. Revenue is recorded when earned following the accrual approach. Expenses are recorded when paid following the cash approach. Some boards use this as a practical middle ground for internal or interim reporting. It gives a better view than pure cash basis without requiring the full infrastructure of accrual. It is not GAAP-compliant, so it should not be used for final annual statements or any reporting that goes to an outside auditor.

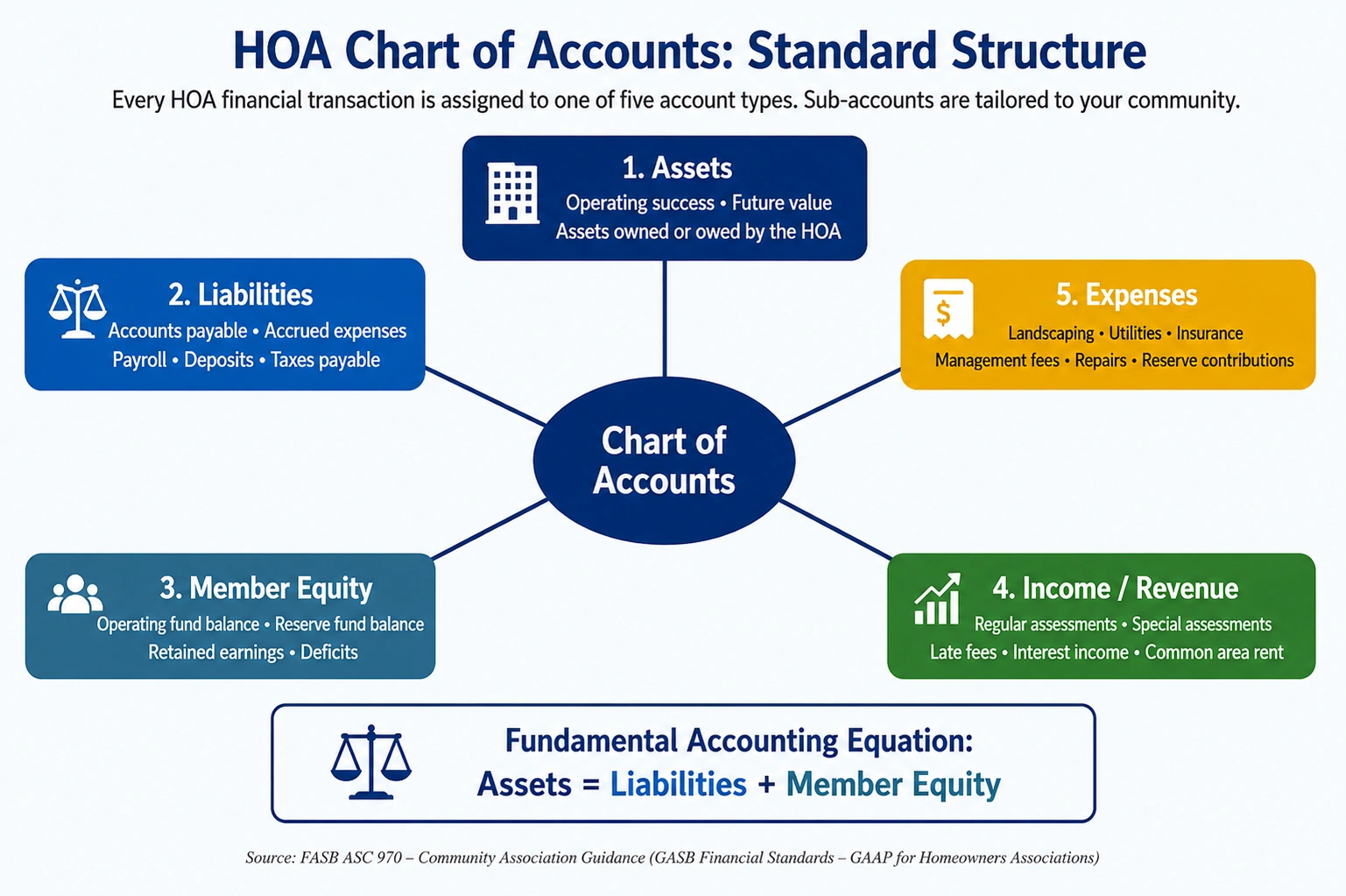

HOA Chart of Accounts

A chart of accounts is the foundation of all HOA bookkeeping. It is a structured list of every financial category your association uses to record transactions. Every dollar that comes in or goes out is assigned to one of these categories, which is what makes your financial statements readable and auditable.

Without a clearly organized HOA chart of accounts, your general ledger becomes a jumble of unlabeled entries that neither the board nor an outside auditor can interpret. With one, every report you generate traces directly back to a clean set of categories that tell a consistent financial story.

A standard homeowners association chart of accounts is organized into five primary account types:

Each of these five types is broken down into sub-accounts that match your community's specific cost categories. A community with a pool, a gym, and gated entry will have different expense sub-accounts than a small neighborhood with only a shared entrance. The chart of accounts should be tailored to your community from the start and updated when new budget categories are added.

If your association is inheriting a poorly structured set of books or starting from scratch, a professional HOA bookkeeping service or community association accountant can establish a compliant chart of accounts as part of onboarding. Getting this structure right at the beginning saves significant time during audits and year-end reporting.

Member Equity and Fund Balance in HOA Accounting

Member equity also called fund balance or net assets is one of the most important and most frequently misunderstood figures on an HOA balance sheet. It represents the cumulative net worth of the association: the difference between total assets and total liabilities at any given point in time.

In a healthy association, member equity is positive and growing over time, which signals that the community is collecting enough in assessments to cover its operating costs and adequately fund its reserves. Negative member equity is a serious warning sign. It usually indicates one or more of the following: the association has been spending beyond its budget for multiple years, reserve contributions have been consistently underfunded, or a significant uninsured expense has depleted the association's financial cushion.

HOAs typically maintain separate fund balances for the operating fund and the reserve fund. These must always be tracked independently and never commingled. The operating fund balance reflects the net of day-to-day income and expenses. The reserve fund balance reflects contributions accumulated for long-term capital expenditures minus amounts spent on reserve projects.

When reviewing your monthly balance sheet, the fund balance lines tell you at a glance whether the association is financially ahead of or behind where it needs to be. A board that understands its fund balance can make informed decisions about assessment levels, capital project timing, and whether a reserve study update is overdue.

Key point: Surplus funds from the operating budget flow into member equity and increase the fund balance. Deficits do the opposite. Over multiple years, the pattern of surpluses and deficits in your fund balance tells the real financial story of how the association has been managed.

Operating Fund vs. Reserve Fund: The Core Financial Structure

One of the most important concepts in HOA management accounting is keeping two pools of money separate: the operating fund and the reserve fund. Treating them as one account is one of the most common financial mistakes HOAs make, and one of the most expensive.

The Operating Fund

One of the most important concepts in HOA management accounting is keeping two pools of money separate: the operating fund and the reserve fund. Treating them as one account is one of the most common and most costly financial mistakes HOAs make.

The operating fund

The operating fund handles the day-to-day costs of running the association. Landscaping, utilities for common areas, insurance, management fees, minor repairs, and administrative expenses all come out of here. Operating budgets are typically set annually, with monthly assessment contributions covering expected costs. Good HOA budget planning reduces the chances of disruptive reserve draws and surprise special assessments.

The reserve fund

Reserve funds are where the association saves for big, infrequent capital expenditures: replacing the roof, repaving parking lots, overhauling the HVAC system, replastering the pool. A reserve study, conducted by an independent professional every three to five years, analyzes the useful life and replacement cost of every major component and tells you how much to set aside each month. Many states now require reserve studies on specific schedules. Underfunded reserves are consistently the primary trigger for the large special assessments homeowners dread. See the guide on HOA reserve funds for a full breakdown of funding strategies and state requirements.

Reserve funding levels explained

Associations are generally described in one of three reserve funding categories:

• Fully funded: reserve balance is at or near 100% of the theoretical ideal calculated by the reserve study. This is the safest position and the one most experienced HOA accounting advisors recommend as the long-term goal.

• Threshold funded: balance is kept above a defined minimum floor. Less aggressive than full funding but still provides meaningful protection against unplanned assessments.

• Baseline funded: the minimum contribution needed to avoid a zero balance. This carries the most financial risk and is the most common trigger for emergency special assessments.

State attention to reserve adequacy has grown sharply in recent years, particularly after high-profile structural failures in condominium communities. Several states have enacted or are actively considering legislation requiring reserve studies on mandatory timelines and setting minimum funding thresholds.

Essential HOA Financial Reports

Professional HOA bookkeeping services generate a standard set of financial statements every month. Board members do not need to be accountants to read them, but they do need to know what each report is showing and what questions to ask when something looks off.

Balance Sheet

The balance sheet is a financial snapshot: what the association owns (assets), what it owes (liabilities), and the difference between the two (member equity or fund balance). Assets include cash in the operating and reserve accounts, assessments receivable, and any investments. Liabilities include accounts payable, accrued expenses, and any outstanding loans. A healthy balance sheet is one of the clearest indicators of HOA financial transparency and the first thing homeowners and auditors look at when evaluating how well the association is managed.

Income statement (profit and loss)

The income statement compares what your association budgeted to what actually came in and went out during a given period, typically month-to-date and year-to-date. The variance column is where the real insight lives. A line item running significantly over budget is a prompt for investigation. One running significantly under budget might mean work is being deferred, which does not make the cost go away.

Cash flow statement

Cash flow answers a simple but critical question: does the HOA have enough cash right now to meet its obligations? An association can look fine on the income statement while running low on cash if assessment collection is slow and vendor payments are due. This report is especially important to watch ahead of large capital projects.

General ledger

The general ledger is the underlying record of every single transaction, posted in full detail. It is the source of truth behind every other report. When discrepancies arise or audit questions come up, this is where accountants and auditors go to trace an issue back to its origin. A well-organized chart of accounts makes the general ledger readable; a poorly organized one makes it nearly impenetrable.

Assessments receivable and delinquency report

Since HOA revenue depends almost entirely on homeowner assessments, knowing who is current and who is not is operationally critical. The delinquency report shows which units are behind, by how much, and for how long. Most governing documents spell out a collections timeline: when late fees accrue, when accounts go to a collections attorney, and when liens are filed on delinquent properties. For a full walkthrough of the assessment collection process and HOA lien procedures, see Effective Strategies for Recovering Delinquent HOA Dues.

Bank reconciliation

Bank reconciliation is the process of comparing your association's internal records to the actual bank statements, line by line, every month. It catches errors before they compound: uncashed checks, duplicate payments, missed deposits, and occasionally unauthorized activity. A board member who does not handle payments should review the reconciliation report each month. This single habit is one of the most effective safeguards an HOA has against both error and fraud.

GAAP and the Regulatory Framework

Generally Accepted Accounting Principles, established by the Financial Accounting Standards Board (FASB) under Accounting Standards Codification 972 (ASC 972), set the standard for how HOA financial statements should be prepared and presented. Four core GAAP principles apply across all compliant HOA reporting:

• Regularity: all financial statements follow established GAAP rules consistently.

• Consistency: the same accounting methods are used from one period to the next, so results can be compared meaningfully over time.

• Sincerity: financials reflect the true condition of the association, without manipulation or selective reporting.

• Accuracy: assets are recorded at their original cost and adjusted appropriately for depreciation over time.

Beyond federal GAAP standards, state laws add requirements that vary considerably by jurisdiction. California, Florida, Texas, and Nevada are among the states with specific legislation covering HOA financial reporting, reserve funding, audit frequency, and disclosure to homeowners. Boards working with professional homeowners association accounting services should confirm their provider is current on their state's specific requirements.

Audits, reviews, and compilations

An audit is an independent examination of the association's financial records by a licensed CPA. It provides the highest level of assurance that your financials are accurate and free from material error. A review provides limited assurance and costs less, making it appropriate for smaller associations or periodic checks between full audits. A compilation is the lowest level, where the CPA organizes the association's records without providing any assurance of accuracy.

The general recommendation is at minimum an external review every one to four years, depending on your governing documents and state. For associations managing substantial reserve funds, an annual audit is the right standard.

HOA Accounting Requirements by State: Key Rules at a Glance

HOA financial reporting requirements, reserve study mandates, and audit obligations vary significantly by state. The following table summarizes key rules for the most active HOA markets. Always confirm current requirements with a local community association attorney or CPA, as statutes change frequently.

Note: This table is a summary reference only and is not legal advice. HOA financial reporting requirements change frequently. Always verify current rules with a licensed community association attorney or a CPA familiar with your state's HOA statutes.

HOA Accounting Services: Self-Managed vs. Professional Management

Every HOA board eventually faces the question of whether to manage the books in-house or bring in a professional HOA management accounting firm. Both approaches can work, but the right answer depends heavily on the size and complexity of your association.

Self-Managed Accounting

Smaller associations with simple financials, a volunteer treasurer who genuinely understands accounting, and limited common area infrastructure sometimes handle their own books well. The risks are real, though. When a knowledgeable treasurer leaves the board, institutional knowledge often walks out the door. When the same person authorizing payments is also reconciling accounts, the risk of errors and fraud increases significantly. And when board members lack accounting backgrounds, problems in the financial records can go unnoticed for months.

Professional HOA Bookkeeping Services

Professional HOA bookkeeping services give associations an accounting infrastructure that most volunteer boards cannot replicate on their own. The right HOA accounting software delivers many of these capabilities in one place. A qualified firm typically delivers:

• Monthly financial packages: balance sheet, income statement, cash flow statement, and variance analysis against budget.

• Assessment collection management: dues billing, payment processing, delinquency tracking, and collections coordination.

• Accounts payable: vendor invoice review, payment authorization, and disbursement.

• Monthly bank reconciliation with board review.

• Reserve fund accounting and investment tracking.

• Annual pro forma budget preparation support.

• Audit coordination and CPA liaison for annual reviews.

The cost of professional HOA accounting services varies with the size of the association, transaction volume, and scope of services. For most boards, the investment is worthwhile not just for the quality of reporting, but for the risk reduction. Accounting errors in HOAs are more common than most people expect, and fraud in self-managed associations is not rare. The board member hours consumed by in-house financial management are a real cost too, even when they do not appear on the budget.

Budgeting and Long-Term Financial Planning

An HOA budget is more than a list of expenses. It is the financial plan that determines what homeowners pay, what the community can afford to maintain, and how prepared the association will be for the capital needs of the next decade. For a deep dive into the full process, the complete guide to HOA financial planning covers everything from gathering historical data to calculating per-unit assessments.

The Annual Budget Process

Most governing documents require boards to adopt a budget before the fiscal year begins, with advance notice to homeowners. A well-built budget starts with a thorough review of the prior year: what was budgeted, what was actually spent, where variances occurred, and why. From there, known cost changes for the coming year are factored in, including contractor renewals, insurance rate adjustments, and utility increases.

Operating expenses are projected line by line. Reserve contributions are determined by the current reserve study. Add those two numbers together, divide by the number of assessment units, and you have the required per-unit assessment. If that number represents a significant jump, the board has options: find savings elsewhere, phase in the increase over two or more years, or accept a higher risk of needing a special assessment down the road.

Reserve Study and Funding Adequacy

A reserve study is the long-term financial backbone of any well-run association. An independent reserve specialist inspects every major common area component, evaluates its current condition and remaining useful life, estimates the cost to replace it, and calculates the annual contribution needed to cover those replacements without interruption.

Associations are generally described as fully funded (reserve balance near 100% of the theoretical ideal), threshold funded (balance kept above a minimum floor), or baseline funded (the minimum to avoid a zero balance, which carries the most risk). Most experienced HOA accounting advisors recommend threshold funding at minimum, with full funding as the goal for newer or higher-value communities.

State attention to reserve adequacy has grown sharply in recent years, particularly after high-profile structural failures in condominium communities. Several states have passed, or are actively considering, legislation requiring reserve studies on mandatory timelines and setting minimum funding thresholds. Boards that have run lean on reserves may face difficult budget conversations with homeowners as these rules take effect.

HOA Tax Considerations

Homeowners associations are not automatically tax-exempt, and the tax treatment of HOA income is more nuanced than many boards realize. Most associations file under one of two federal returns: Form 1120-H, which is specific to homeowners associations under IRC Section 528, or Form 1120, the standard corporate return.

Form 1120-H is the more common choice. Under this filing, membership income, which includes dues, regular assessments, and most fees paid by homeowners, is generally exempt from federal income tax. Non-exempt income is taxable at a flat 30% rate. Non-exempt income includes interest earned on reserve fund investments, income from renting common facilities to non-members, and income from cell tower leases. For timeshare associations, the non-exempt rate is 32%.

Form 1120 does not provide the same membership income exemption, but it allows deductions that 1120-H does not. For associations with substantial non-exempt income, a CPA who specializes in HOA taxation should model both approaches before deciding which return to file.

State tax obligations are a separate question entirely. Some states treat HOAs as tax-exempt; others require state corporate returns on top of the federal filing. Property tax treatment of common areas also varies by state and is not automatic. A local tax professional familiar with community association law is the right resource for understanding your specific obligations.

Internal Controls and Fraud Prevention

Fraud in homeowners associations is more common than most people assume. Embezzlement by volunteer treasurers, management company employees, and even board members surfaces in the news regularly. The answer is not simply hiring people you trust. It is building a structure where fraud is difficult to commit and easy to detect. Building a clear HOA transparency strategy is one of the most effective ways to prevent it before it starts.

The most important internal controls for HOA accounting include:

• Separation of duties: the person who authorizes expenses should never be the same person who issues checks or processes online payments.

• Dual signatures required on checks above a set threshold, commonly $1,000 or $2,500.

• Monthly bank statements reviewed by a board member who has no payment authority.

• Competitive bidding requirements for contracts above a specified dollar amount.

• Annual rotation of account signatories as board members change.

• Fidelity bond (crime insurance) coverage for all individuals who handle association funds. Many governing documents require this; all associations should have it.

• Online account access limited on a need-to-know basis, protected by multi-factor authentication.

One of the underappreciated benefits of engaging professional homeowners association accounting services is the built-in separation of duties they provide. When accounting is handled by an outside firm, the financial function is structurally separate from the board, which makes certain types of fraud significantly harder to carry out and easier to catch.

Technology and the Future of HOA Accounting

HOA management accounting has changed more in the past five years than in the previous twenty. Cloud-based platforms, automated payment tools, and real-time reporting have raised the bar for what boards and homeowners can reasonably expect from their association's financial operations.

Cloud-Based Accounting Platforms

Modern HOA accounting software, whether a general-purpose platform like QuickBooks Online or a purpose-built community association solution, gives boards on-demand access to financial data rather than waiting for a monthly report package. Homeowners can log in to check their account status, make payments, and view association financials through a portal. That kind of transparency reduces friction and builds trust.

Automated Payment Processing

ACH payments, automated recurring dues charges, and electronic check processing have made dues collection faster and more predictable. When paying dues is convenient, late payment rates go down. When fewer paper checks are in circulation, reconciliation becomes simpler and the risk of manual errors decreases.

AI and Automation

Artificial intelligence is beginning to show up in HOA accounting workflows, mainly in automated data entry, anomaly detection in transaction records, and predictive budgeting tools that flag unusual spending patterns or project reserve fund trajectories under different scenarios. These tools are still developing, but early adopters in the community association management space are already seeing meaningful efficiency gains.

Cybersecurity

As more HOA financial activity moves online, cybersecurity has become a genuine operational concern. Wire fraud targeting community associations has increased substantially in recent years. The typical attack involves criminals intercepting payment communication and redirecting funds to a fraudulent account. Associations and their accounting service providers need clear protocols for verifying any change to payment instructions, multi-factor authentication on all financial accounts, and appropriate cyber liability insurance coverage.

Choosing the Right HOA Accounting Partner

For boards evaluating HOA accounting services or homeowners association accounting services, the decision involves a lot more than comparing monthly fees. A qualified accounting partner should bring:

• Hands-on experience with community association accounting, not just general business bookkeeping.

• A standardized monthly financial package delivered on a predictable schedule.

• Responsive communication and the ability to explain specific line items clearly when the board has questions.

• Technology that gives board members and homeowners access to financial data without having to request it.

• Solid working knowledge of your state's HOA financial reporting and reserve requirements.

• Audit support and the ability to coordinate with the association's CPA for annual reviews.

• Transparent, straightforward pricing with no surprise fees for standard reporting.

• Tax preparation and filing, including Form 1120-H or Form 1120 as appropriate.

One of the underappreciated benefits of engaging professional homeowners association accounting services is the built-in separation of duties. When accounting is handled by an outside firm, the financial function is structurally separate from the board, which makes certain types of fraud significantly harder to carry out and easier to detect. Boards that have experienced fraud or accounting irregularities in self-managed settings often cite this structural separation as the primary reason they switched to professional services.

HOA Accounting Cost: What to Expect in 2026

One of the most common questions boards ask when evaluating HOA bookkeeping services is what professional accounting actually costs. The answer depends on the size of the association, transaction volume, scope of services, and geographic market. Here are the verified 2026 ranges based on industry data.

These ranges reflect monthly bookkeeping services only. Separate fees typically apply for annual audits (typically $2,000 to $8,000 for a full CPA audit depending on association size), tax return preparation ($300 to $1,500), and reserve study updates ($1,500 to $5,000 every three to five years).

When comparing HOA accounting fees, boards often focus only on the monthly rate. The more useful comparison is total annual cost against the risk profile of self-management, including the cost of a bookkeeping error, a missed tax deadline, or the audit hours required to untangle messy records. For most associations with more than 50 units, professional accounting services deliver a clear return through time savings, error reduction, and stronger financial oversight.

Source: HOA accounting cost ranges verified against OJO Bookkeeping 2026 fee guide, Hillcrest HOA Management, and multiple industry sources. Actual costs vary by market and service scope.

Budgeting and Long-Term Financial Planning

An HOA budget is more than a list of expenses. It is the financial plan that determines what homeowners pay, what the community can afford to maintain, and how prepared the association will be for the capital needs of the next decade. For a deep dive into the full process, the complete guide to HOA financial planning and budgeting covers everything from gathering historical data to calculating per-unit assessments.

The annual budget and pro forma process

Most governing documents require boards to adopt a budget before the fiscal year begins, with advance notice to homeowners. In states like California, the budget must be presented as a pro forma operating budget a projected forward-looking statement of expected income and expenses prepared in accordance with accrual accounting principles.

A well-built budget starts with a thorough review of the prior year: what was budgeted, what was actually spent, where variances occurred, and why. From there, known cost changes for the coming year are factored in: contractor renewals, insurance rate adjustments, and utility increases. Operating expenses are projected line by line. Reserve contributions are determined by the current reserve study. Add those two numbers together, divide by the number of assessment units, and you have the required per-unit assessment for the coming year.

Reserve study and funding adequacy

A reserve study is the long-term financial backbone of any well-run association. An independent reserve specialist inspects every major common area component, evaluates its current condition and remaining useful life, estimates the cost to replace it, and calculates the annual capital expenditure contribution needed to cover those replacements without interruption.

HOA Tax Considerations

Homeowners associations are not automatically tax-exempt, and the tax treatment of HOA income is more nuanced than most boards realize. Most associations file under one of two federal returns: Form 1120-H or Form 1120.

Form 1120-H and IRC Section 528

Form 1120-H is the more common filing choice. It is available to qualifying homeowners associations under Internal Revenue Code Section 528 (IRC Section 528). Under this provision, membership income which includes regular assessments, dues, and most fees paid by homeowners for community purposes is exempt from federal income tax. Non-exempt income is taxed at a flat 30% rate (32% for timeshare associations).

To qualify for 1120-H treatment under IRC Section 528, the association must meet several tests: at least 60% of gross income must come from exempt function income (homeowner assessments), at least 90% of expenses must be for the acquisition, construction, management, maintenance, or care of association property, and no private shareholder or individual may benefit from the association's net earnings.

Non-exempt income that does not qualify for exclusion under IRC Section 528 includes: interest earned on reserve fund investments, income from renting common facilities to non-members, and income from cell tower leases or other commercial arrangements. These amounts are taxable at the 30% flat rate on Form 1120-H, regardless of how much the association may have spent on exempt activities.

Form 1120

Form 1120, the standard corporate return, does not provide the same membership income exemption as 1120-H. However, it allows deductions that 1120-H does not, and for associations with substantial non-exempt income, a CPA who specializes in HOA income tax exemption issues should model both approaches before deciding which return to file. The deadline for both forms is typically April 15, or the 15th day of the 4th month after the association's fiscal year ends.

State tax obligations are a separate question entirely. Some states treat HOAs as tax-exempt; others require state corporate returns on top of the federal filing. Property tax treatment of common areas also varies by state and is not automatic. A local tax professional familiar with community association law is the right resource for understanding your specific obligations.

Internal Controls and Fraud Prevention

Fraud in homeowners associations is more common than most boards assume. Embezzlement by volunteer treasurers, management company employees, and board members surfaces in the news regularly. The answer is not simply hiring people you trust. It is building a structure where fraud is difficult to commit and easy to detect. Building a clear HOA transparency strategy is one of the most effective preventive measures an association can take.

The most important internal controls for HOA accounting include:

• Separation of duties: the person who authorizes expenses should never be the same person who issues checks or processes online payments.

• Dual signatures: required on checks above a set threshold, commonly $1,000 or $2,500.

• Independent bank statement review: a board member with no payment authority should review bank statements and the reconciliation report each month.

• Competitive bidding requirements: for contracts above a specified dollar amount, typically $5,000 or $10,000.

• Fidelity bond (crime insurance): coverage for all individuals who handle association funds. Many governing documents require this; all associations should carry it.

• Limited online account access: protected by multi-factor authentication and restricted on a need-to-know basis.

• Annual vendor list review: confirm all active vendors are legitimate and that no payments are going to unauthorized parties.

Technology and HOA Accounting Software

HOA management accounting has changed significantly in the past five years. Cloud-based platforms, automated payment tools, and real-time reporting have raised the bar for what boards and homeowners can reasonably expect from their association's financial operations.

HOA accounting software and cloud platforms

Modern HOA accounting software - whether a general-purpose platform like QuickBooks Online adapted for community associations, or a purpose-built community association solution gives boards on-demand access to financial data rather than waiting for a monthly report package. Homeowners can log in to check their account status, make payments, and view association financials through a homeowner portal. That kind of transparency reduces friction and builds trust in ways that paper-based reporting never could.

When evaluating HOA accounting software, boards should look for: a chart of accounts structured for community associations, integrated assessment billing and payment processing, reserve fund tracking separate from operating accounts, bank reconciliation tools, financial statement generation with budget variance reporting, and audit trail capabilities. Software that connects directly to your bank accounts reduces manual entry and the errors that come with it.

Automated assessment collection

ACH payments, automated recurring dues charges, and electronic check processing have made assessment collection faster and more predictable. When paying dues is convenient, late payment rates decrease. When fewer paper checks are in circulation, reconciliation becomes simpler and the risk of manual errors goes down. For larger associations, automated collection workflows can also flag delinquencies automatically and trigger the first steps of the collections process without manual intervention.

AI and automation in HOA bookkeeping

Artificial intelligence is beginning to appear in HOA accounting workflows, mainly in automated data entry, anomaly detection in transaction records, and predictive budgeting tools that flag unusual spending patterns or project reserve fund trajectories under different scenarios. Early adopters in the community association management space are already reporting meaningful efficiency gains, particularly in the time spent on month-end close and financial reporting preparation.

Cybersecurity for HOA finances

As more HOA financial activity moves online, cybersecurity has become a genuine operational concern. Wire fraud targeting community associations has increased substantially in recent years. The typical attack involves criminals intercepting payment communication and redirecting funds to a fraudulent account. Associations and their accounting service providers need clear protocols for verifying any change to payment instructions, multi-factor authentication on all financial accounts, and appropriate cyber liability insurance coverage.

Choosing the Right HOA Accounting Partner

For boards evaluating HOA accounting services or homeowners association accounting services, the decision involves far more than comparing monthly fees. A qualified accounting partner should bring:

• Hands-on experience with community association accounting, not just general business bookkeeping.

• A standardized monthly financial package delivered on a predictable schedule.

• Responsive communication and the ability to explain specific line items clearly when the board has questions.

• Technology that gives board members and homeowners access to financial data without having to request it.

• Solid working knowledge of your state's HOA financial reporting and reserve requirements.

• Audit support and the ability to coordinate with the association's CPA for annual reviews.

• Transparent, straightforward pricing with no surprise fees for standard reporting.

The best accounting relationships are collaborative. Boards that read their monthly reports, ask questions about variances, and hold their accounting firm accountable for accuracy and timeliness get far better outcomes than boards that rubber-stamp what is in front of them. The financials are a management tool, and treating them that way makes a real difference in how a community performs over time.

HOA Accounting Best Practices: Quick Reference

• Use accrual basis accounting for all formal financial statements and reserve reporting.

• Establish and maintain a properly structured HOA chart of accounts from day one.

• Keep operating and reserve funds in separate accounts and never commingle them.

• Conduct a professional reserve study every three to five years and update annually.

• Review monthly financial statements as a board balance sheet, income statement, bank reconciliation, and delinquency report.

• Implement separation of duties so no single person controls both payment authorization and account reconciliation.

• Maintain a fidelity bond covering all individuals with access to association funds.

• File Form 1120-H annually by the April 15 deadline and track non-exempt income separately throughout the year.

• Conduct a CPA review or audit at least every one to four years, or annually for larger associations.

• Keep the chart of accounts current as community cost categories evolve.

Conclusion

Good community association accounting does not happen by accident. It takes the right method, the right chart of accounts structure, the right internal controls, and the right people reviewing the numbers with enough regularity to catch problems early. When all of that is in place, the financial side of association management becomes something the board can rely on rather than worry about.

The tools available today make it more achievable than ever. Professional HOA bookkeeping services bring a level of accuracy and consistency that most volunteer boards cannot replicate on their own. Cloud-based HOA management accounting platforms give boards real-time visibility that was simply not possible a decade ago. And while state regulations are getting stricter, those requirements are also pushing the entire industry toward better practices that ultimately benefit homeowners.

Whether your community works with a full-service homeowners association accounting services provider or manages the books internally with strong controls and qualified oversight, the commitment to financial transparency is not negotiable. ManageCasa HOA accounting software gives boards the real-time reporting, automated payments, and audit-ready financials to make that commitment easier to keep.

Frequently Asked Questions

What accounting method should an HOA use?

Most HOAs should use accrual basis accounting for formal financial statements and reserve reporting. It is the only method that conforms with GAAP, provides accurate tracking of assessments receivable and accounts payable, and is accepted for audited financial statements. Smaller associations sometimes use cash basis for simplicity, but it does not provide a complete picture of the association's financial position and is not acceptable for reviewed or audited financials.

What is an HOA chart of accounts?

A chart of accounts is a structured list of every financial category your association uses to record transactions. It is organized into five primary types: assets, liabilities, member equity / fund balance, income, and expenses. Each category is broken into sub-accounts that match your community's specific cost structure. A properly organized chart of accounts is the foundation of accurate HOA bookkeeping and makes financial statements readable and auditable.

What is the difference between an HOA operating fund and a reserve fund?

The operating fund covers day-to-day expenses such as landscaping, utilities, insurance, and management fees. The reserve fund is set aside for major long-term capital expenditures like roof replacement, repaving, or equipment upgrades. These funds must be kept in separate accounts and cannot be commingled. Most state HOA laws require associations to maintain reserve funds and, in many states, to commission a reserve study to verify adequate funding levels.

What financial reports should an HOA produce each month?

At a minimum, HOA boards should review a balance sheet, an income and expense statement compared to budget, a delinquency report showing unpaid assessments, and a bank reconciliation confirming account balances match bank records. Reserve fund balance and contribution tracking should also be reviewed regularly. These reports give the board visibility into financial health and flag issues before they become serious problems.

How much does HOA accounting cost?

Professional HOA bookkeeping services typically cost $200 to $500 per month for small associations under 50 units, $500 to $1,500 per month for mid-size associations of 50 to 200 units, and $1,500 to $3,000 or more per month for large associations. Additional fees apply separately for annual CPA audits, tax return preparation, and reserve study updates. Total annual accounting cost for a mid-size association with professional services typically runs $6,000 to $18,000.

Expert in Property Management and SaaS

Peter Koch is an expert in property management and SaaS, focused on building top digital tools for property managers and growing technology-driven startups. He specializes in enhancing property management operations through smart software solutions that streamline accounting, automate workflows, and improve community communication. Peter writes about HOA management technology, proptech innovation, and scalable SaaS strategies designed to help modern property professionals operate more efficiently.